Summary

- Exxon Mobil has seen a considerable decline since mid-April.

- Macroeconomic concerns are plentiful, but none cater to disruptions in crude oil to supply at this time.

- Sustained lower commodity prices weighs on the earnings potential of the company and despite the high yield, investors should look elsewhere.

Exxon Mobil (XOM) has revisited six-month lows on the back of falling commodity prices and the lure of a near 5% yield draws near. Investors should entirely avoid this yield as the macroeconomic backdrop is simply not supportive of an investment in the major integrated oil and gas space at this time. With the ongoing trade war and high U.S. production levels resulting in inventory builds rather than draws, the fundamentals aren't positive and I believe further downside is warranted for both crude oil and natural gas prices, as well as Exxon Mobil shares.

Source: Houston Chronicle

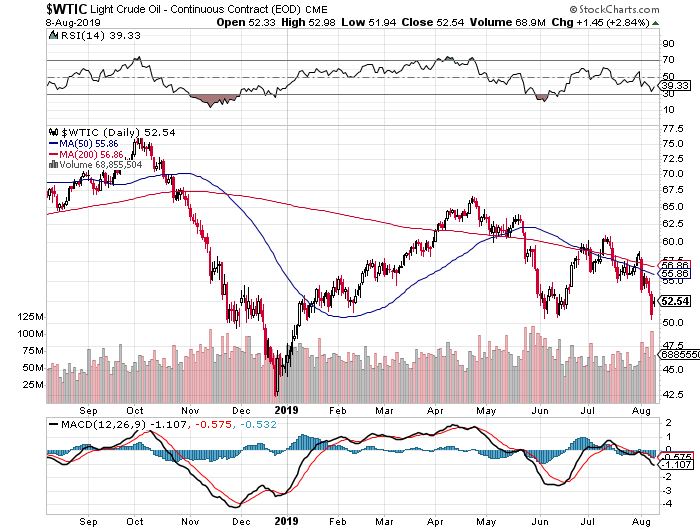

Lower Commodity Pricing Remains An Issue

Crude oil has really taken a turn for the worse in late Q2 and recently in late July/early August as U.S. production remains quite strong, inventory builds are taking the place of expected withdrawals, and global trade tensions aren't resulting in supply disruptions as investors had hoped for. At a high level, the August decline has been driven by a fear over a loss of demand from China, given the rising trade war tensions, and related fears that global growth is slowing.

Source: StockCharts

Source: StockCharts

Investors should have the base case for multinational equities that a resolution to the trade war will drive asset prices higher and that includes crude oil, the primary driver for XOM shares. The heightened tariffs and even the threat of heightened tariffs make crude oil futures unattractive to own, given the negative impact on potential economic growth. However, it's also important that investors keep an eye on API and EIA-reported data, as the reversal to builds before the summer driving season ends is a roadblock for those bullish on crude oil.

For example, this week we've seen a build of 2.4 million barrels in U.S. stockpiles vs. a 2.8 million barrel draw. That's a net differential of 5.2 million barrels and the magnitude of a differential tends to rattle investor confidence. The path of least resistance is down for crude oil and while there will be substantial support for WTI at $50/barrel, the lower asset prices drive down the earnings potential for the quarter for Exxon Mobil.

I've seen discussion of OPEC potentially supporting oil prices with further cuts or a longer period of lower production levels. While I don't doubt the abilities of OPEC to reduce production levels, as well as follow-up with rhetoric that may provide short-term support for commodity prices, the organization has to wait until September 12, when their next meeting takes place, in order to actually follow through with any sort of action. Until then, expectations are free to be set where they may and the OPEC chatter sits in the background against an escalated trade war and a reversal in trend for U.S. inventories.

The company has also been negatively impacted by falling natural gas prices. The acceleration to the downside that natural gas prices have seen since December has been quite the spectacle to observe. This has led to lower gas realizations and a consequential negative effect on the LNG business. Below is a one-year chart of natural gas and investors can see how almost bubble-like the run-up in December proved to be. A sub-$2/MMBtu pricing on the Henry Hub would be something that hasn't been seen in quite some time, but the fact of the matter is that the commodity is approaching that mark and it has a severe impact on Exxon Mobil. Both the company's natural gas E&P operations and its LNG operations, albeit the latter is on a lag, see pricing weakness and that translates to earnings weakness. Even just this quarter, natural gas pricing looks to have deteriorated by 7%, on average.

{kind=link}