Summary

- Although the pandemic brings certain risks, the downtrend in office visits and elective procedures more than compensates for COVID related costs.

- The acquisition of Express Scripts grew revenues and debt by wide margins.

- Growth initiatives coupled with PBM synergies should propel revenue growth.

- I find myself in a bit of a predicament. My area of expertise is dividend growth stocks. As an investor, I travel the buy and hold, slow but sure road to investment success.

While Cigna Corporation (CI) is technically a dividend bearing stock, a yield of .02% does not warrant my interest. However, capital gains are of importance to me, and bulls believe Cigna will outperform the market.

Of course, there is also a bear side to Cigna's story.

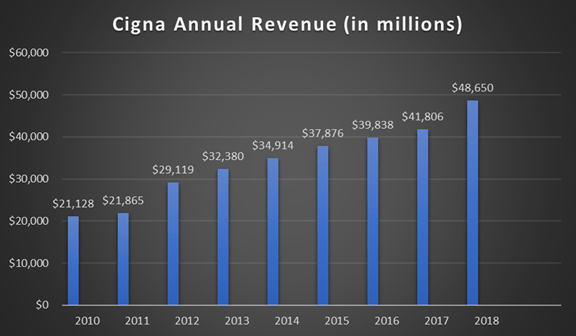

This, however, is not open to debate: Cigna's business has grown rapidly over the last decade. The following chart testifies to the increase in revenues over the years.

Source: Metrics from Macrotrends/Chart by Author

You might note that the year 2019 is missing. That is due to last year's tremendous growth in revenues to $153,566,000,000, more than triple 2018's sum.

So why is the stock trading nearly 20% below its 52 week high?

Naysayers will point to the specter of Medicare for All, a degree of client concentration risk, the recent loss of the company's largest PBM customer, Anthem (ANTM), integration risk associated with the company's acquisition of Express Scripts, and headwinds associated with the COVID crisis.

Bulls view the coronavirus developments as net neutral and praise a variety of initiatives and developments that should lead to a bright future for investors.

Pandemic Problems

The Department of Health and Human Services ruled that testing for coronavirus is an essential health benefit. Consequently, insurers must cover the costs.

Bloomberg estimated the price of commercial tests will range between $50 and $100. Assuming $100 per test and that 10% of the population is tested, we arrive at a system wide cost of approximately $3.1 billion.

Obviously, Cigna would not bear the entire burden. While testing and treatment related to COVID will be a drag on providers revenues, those costs are more than offset by other developments.

The pandemic caused the cancellation of many elective procedures resulting in fewer claims. In turn, this leads to a profit boost for insurers.

For example, HCA Healthcare (HCA), the largest for-profit hospital operator in the US, reported a 70% drop in outpatient surgeries and a 30% decline in inpatient admissions compared to last year.

Employers reported a 30% to 40% reduction in healthcare uses, not including visits related to COVID-19.

...testing is a drop in the bucket compared to all the surgeries that didn't happen...

Ben Isgur, PwC's Health Research Institute,

Another COVID related concern is workforce reductions of companies that are clients of Cigna's. Approximately 85% of Cigna's customers are large employers. Management stated only half of employer layoffs result in benefit disruption, implying companies anticipate a return of those workers.